Industry Insights - Metal

India’s metal industry is expanding as a result of increased automotive and infrastructure development. Compared to May 2020, when 5.8 million tonnes of crude steel were produced, 9.2 million tonnes of crude steel were produced in May 2021, a 46.9% YoY increase. By FY22, it is anticipated that India will produce 120 million tonnes (MT) more steel, an increase of 18%.

In terms of the cost of producing and converting alumina and steel, India has a slight advantage. With a production of 99.6 MT, India is the second-largest producer of crude steel worldwide as of 2020. In FY20, the output of finished steel was 101.03 MT, while the production of crude steel was 108.5 MT. India has a total of 914 steel factories that produced crude steel in FY20. In FY21, India produced 102.49 million tonnes of crude steel. SAIL produced 1.55 MT of hot metal, 1.44 MT of crude steel, and 1.46 MT of saleable steel in September 2021, respectively.

Our Indian metal sector insight covered 10 companies :

- Tata Steel Ltd.

- JSW Steel Ltd.

- Hindalco Industries Ltd.

- Vedanta Ltd.

- NMDC Ltd.

- SAIL Ltd.

- Jindal Steel Ltd

- Gallantt Metal Ltd.

- Ankit Metal and Power Ltd.

- Tata Metaliks Ltd.

Financial Matrices for FY21-22

- A significant increase in the Average Market Cap in FY21 with an overall increase of 227%.

- Falling EBITDA and PAT growth in spite of huge increase in Median Revenue growth.

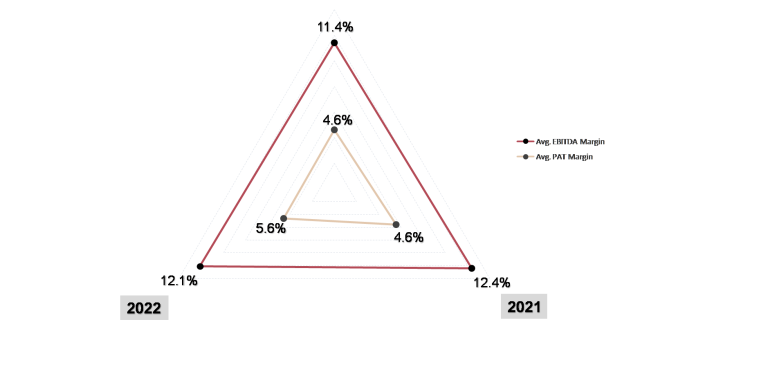

Avg. EBITDA margin has increased significantly in FY21 by 40.5%.

Along with this, PAT margin has also witnessed a drastic increase of 609.5% in FY21.

- Median ROCE rose by 10 times to 14.1% in FY21 and further increased marginally to 15.1% in FY22.

- Average Debt to Capital Employed declined by 95.6% during FY20-22 with TATA Metaliks being debt free for the last 3 years.

- Dip in Cash to revenue Ratio by 10.5% in FY22 and rise in Current Ratio in FY22 by 30 basis points.

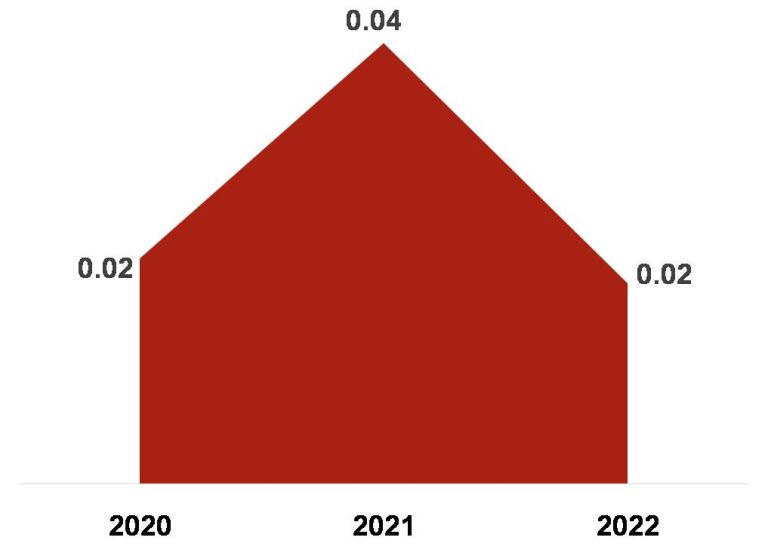

Median P/FCFE rose significantly by 100% (to 0.04%) in FY21 and then fell by 50% (to 0.02%) in FY22.

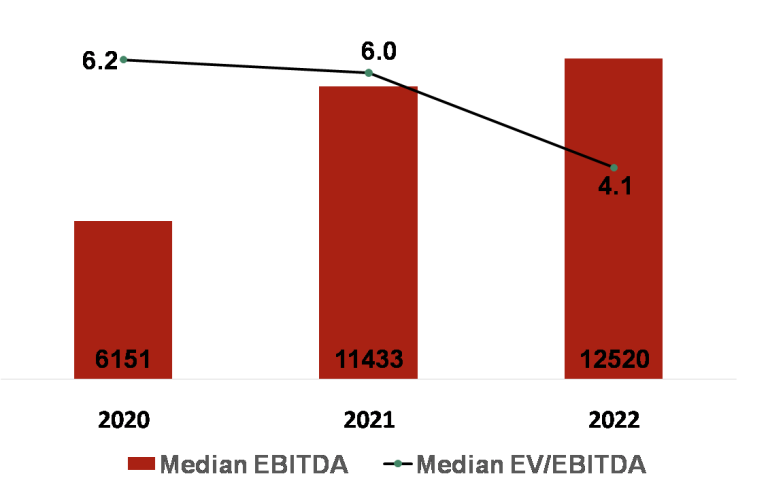

Median EV/EBITDA decreased by 33.87% in FY22 whereases, the EBIDTA grew significantly by 85.87% in FY21 and further increased in FY22.

Median ROE rose substantially to 17.4% in FY21 and fell by 0.7% to 16.7% in FY22.

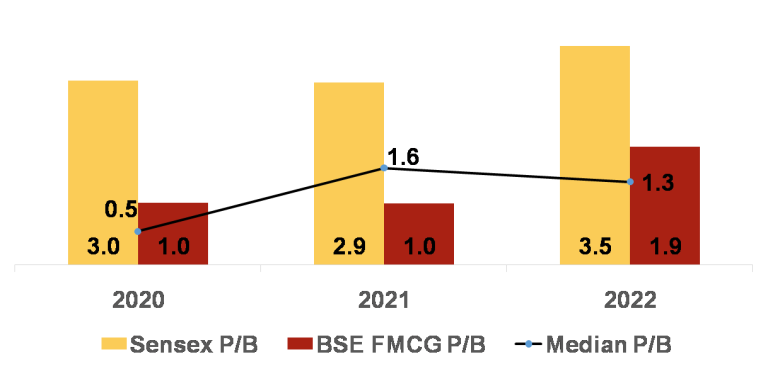

Sensex P/B fell marginally in FY21 and then grew by 20.7% in FY22

BSE Metal P/B grew rapidly witnessing a 90% growth from FY21 – FY22

Median P/B grew immensely by over 220% in FY21 and then fell by 18.75% in FY22

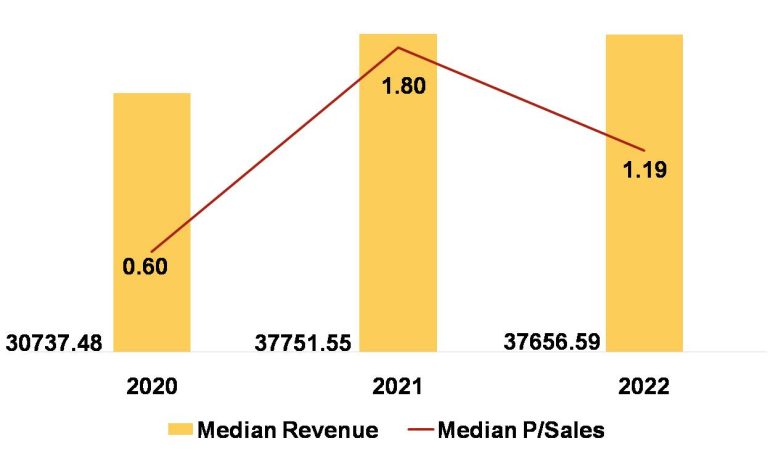

Median TTM P/Sales initially increased and finally decreased in FY21 and FY22. The revenue grew by only 22.5% in FY20-22.

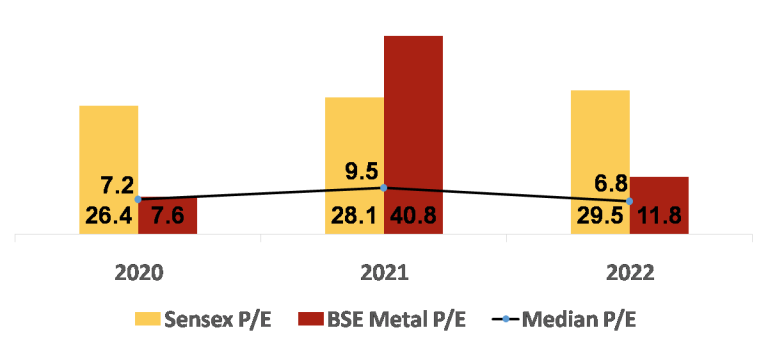

Median P/E multiple fell by 5.6% in FY20-22 but continues to be

higher than Sensex P/E.

Current trends in the Indian Metal sector

Capital:

Metal industry especially, the Iron and steel, requires large capital investment for expenses like setting up of infrastructure for a metal plant; purchasing of heavy machinery and other expenses. Investments like theseare difficult for a developing country like India to afford. Many of the public sector integrated steel plants have been established with the help of foreign aid.

Low Productivity:

The per capita labour productivity in the country is at 90-100 tonnes for the steel industry which is very low. It is 600-700 tonnes per person in Korea, Japan, and other steel producing nations.

Moreover, Durgapur steel plant makes use of approximately 50% of its potential which is caused by factors like strikes, shortage of raw materials, energy crisis, incompetent administration, etc. Due to low productivity, the demand is never met. Thus, huge chunks of steel and other metals are to be imported in order to meet the demands. In order to save invaluable foreign exchange, productivity needs to be increased.

Inferior Quality of Products:

The weak infrastructure, capital inputs and other facilities eventually lead to metallurgical process more time-taking, expensive and produces an inferior variety of alloys. Thus, even if the supply of metal is sufficient, direct consumers of the metal industry prefers to use imported metal products rather than metal products produced in the country.

Looking at the road ahead for the metal industry

The National Steel Policy, 2017 envisage 300 million tonnes of production capacity by 2030-31. The per capita consumption of steel has increased from 57.6 kgs to 74.1 kgs during the last five years. The government has a fixed objective of increasing rural consumption of steel from the current 19.6 kg/per capita to 38 kg/per capita by 2030-31.

Huge scope for growth is offered by India’s comparatively low per capita steel consumption and the expected rise in consumption due to increased infrastructure construction and the thriving automobile and railways sectors.

– Harshadev Sengupta & Sonal Agarwal

Source: bseindia.com

It should be noted that while conducting the analysis, we have NOT conducted the interviews with the managements of companies under review. The contents of this presentation is for understanding and learning purposes only. It should not be treated as professional or investment advice.

For professional enquiries, please email valuation@omnifinsolutions.com