During my two decades of professional experience, I have done hundreds of valuation engagements across fundraises, acquisitions, regulatory filings, disputes, and IPOs. And through all of it, one problem in the valuation of private companies never went away. There is no market to check your answer against.

When you value a listed company, the stock price talks back. It may not always be right, but it forces a conversation. When you value a private company, the only voice in the room is your own model — built on your projections, your discount rate, your terminal assumptions. If those assumptions are optimistic, the output is optimistic, and nothing inside the spreadsheet will ever tell you so.

That gap is what my doctoral research set out to close. The result is the GREV Model — Goel’s Revenue and Earnings based Valuation Model — an empirical benchmark for the valuation of private companies in India, derived from real transaction data rather than theory. This article explains the model, the evidence behind it, and how valuers, investors, and CFOs can put it to work.

Private company valuations – the problem

The three classical approaches — income, market, and cost — remain the foundation of the valuation of private companies. But there are multiple challenges in valuing startups and private companies. But each one struggles in the Indian private market:

The DCF method:

The DCF is only as honest as its projections. Terminal value routinely accounts for the majority of a DCF conclusion, and terminal value rests on assumptions no one can verify today. Add the difficulty of estimating cost of equity for a company with no listed peers — no observable beta, no clean cost of debt — and “projection bias” quietly converts aspiration into valuation.

Comparable companies multiple method

Comparable multiples invite cherry-picking. Genuine comparables for Indian private companies are scarce, disclosures are selective, and it is temptingly easy to choose the peer set that supports the number someone already wants.

The Cost Approach and NAV method

The cost approach misses the point entirely for modern businesses, where value lives in brands, technology, distribution, and scalability — none of which appear on the balance sheet at anything close to economic worth or fair value.

But valuations are done by Registered Valuers

Most valuations are actually bottom-up exercises. The founder or investor (or both) agree on a valuation, deal is closed and the valuer is appointed to back-fill the assumptions to arrive at the agreed value. The actual performance, projected performance and final valuation is all provided by the client – the valuer only calculates the Discount Rate that fills the gap. If you want to do a fair valuation without the bias, the result is almost always the same. Two competent valuers, same company, same date, materially different numbers that doesn’t serve anyone’s purpose.

What the valuation of private companies has lacked is not another method — it is an independent, evidence-based reference point to test whichever method the valuer has used.

What my research actually found

For my PhD, I analysed funding transactions in over 3,900 Indian private companies backed by angel, VC, and PE investors between 2015 and 2024. The question was simple to state and hard to answer: do the valuations investors actually pay bear a measurable statistical relationship to the companies’ financial fundamentals?

To keep the analysis meaningful, the sample was refined to companies with a degree of operating maturity — annual revenue above ₹1 crore and positive EBITDA. After testing multiple specifications, the strongest relationship emerged from a power-law regression on just those two variables.

The finding that matters most: these two numbers alone explain approximately 47% of the variation in private company valuations in India.

Pleasantly surprised. Deal-making is supposedly driven by narrative, chemistry, FOMO, and negotiation. Yet nearly half of what institutional investors actually pay is anchored in two lines of the financial statements. Private market pricing is far more disciplined than its reputation suggests — and far more measurable.

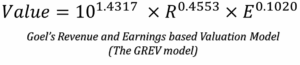

Goel’s Revenue and Earnings Based Valuation Model (The GREV Model)

The fitted equation is:

Value = 10^1.4317 × R^0.4553 × E^0.1020

where Value is the estimated enterprise value, R is revenue, and E is EBITDA — latest period, all in INR crore.

Three insights are embedded in those exponents, and each one carries a lesson for the valuation of private companies:

- Value scales non-linearly with size. The power-law form means a company that doubles its fundamentals more than doubles nothing — value follows scale along a curve, not a line. Larger, stable businesses command a size premium that is baked into actual market pricing behaviour, not merely asserted by valuers.

- Revenue dominates profitability. The revenue exponent (0.4553) is roughly four and a half times the EBITDA exponent (0.1020). Indian private capital prices traction first — the top line is treated as the primary evidence that a business model works and can grow. Operating efficiency matters, but as a secondary anchor.

- The unexplained half is where judgment lives. If 47% of valuation is explained by financials, roughly 53% is driven by everything else: management quality, governance standards, business model strength, market positioning, strategic relevance, scalability, investor confidence, and of course, future projected performance. The model does not eliminate professional judgment — it locates it, and tells you how much of the final number that judgment must carry.

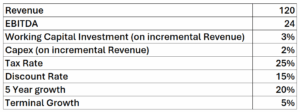

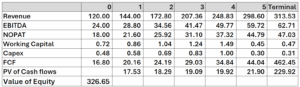

Worked Example:

Let’s consider a hypothetical private company with the following assumptions and a DCF outcome.

The same valuation under the GREV Model would lead to

Value

= 10^1.4317 × R^0.4553 × E^0.1020

= 10^1.4317 x 120^0.4553 x 24^0.1020

= 330.41 Crore

That is, a variation of ~1%. Of course, if the assumptions change, the deviation would keep on increasing as the GREV Model would remain intact with the same level of EBITDA and Revenue. Let’s say that with alternate assumption of 5 Year Revenue growth of 25%, the DCF value came at INR 390 Crore.

Would that mean that either DCF or the GREV Model value is wrong? No — and this is the point most people miss. It means the valuer must now articulate a premium justification: how would the company command a high revenue growth despite a nominal capex and working capital investment? Is it going to leverage Proprietary technology? A contracted order book? Dominant regional share? If the answer is convincing, the report becomes stronger for stating it. If no answer survives scrutiny, the projections were probably optimism wearing a spreadsheet.

That is the discipline GREV attempts to impose. The model never overrules the valuer. It asks the one question a self-referential DCF never will.

How to use GREV in practice

GREV can be a standard calibration step in private company engagements:

Step 1. complete the primary valuation on its own merits — DCF, multiples, or both, exactly as valuation standards require, without reference to the benchmark. The primary method must not be anchored by advance knowledge of where GREV sits.

Step 2. compute the GREV value — thirty seconds with the latest revenue and EBITDA.

Step 3. Interrogate any material gap, in either direction. A DCF well above GREV demands a premium justification. A DCF well below it raises the mirror question: excessive conservatism, or a genuine impairment — customer concentration, regulatory overhang, related-party dependence — that market-wide data cannot see?

This workflow also strengthens the valuation of private companies under scrutiny. Ind AS 113 and the International Valuation Standards consistently favour observable, market-corroborated inputs over unobservable ones. Where a fair value conclusion rests heavily on Level 3 inputs, an empirical benchmark derived from thousands of actual transactions moves the conversation toward market-anchored evidence i.e. Level 2 input. In our experience, audit committees, Big 4 reviewers, and regulators respond very differently to a conclusion that arrives with an independent statistical cross-check than to one defended purely on assumption quality.

Limitations of GREV Model

I built this model, so let me be the first to state its boundaries plainly.

GREV is a benchmarking and calibration tool, not a standalone valuation method. No Registered Valuer should sign a conclusion that rests on a regression output — and none should need to, because the model’s role is to test conclusions, not produce them.

It applies to Indian private companies with revenue above ₹1 crore and positive EBITDA. Cash-burning early-stage startups sit outside its design, as do situations requiring equity-level adjustments the enterprise-value formulation does not capture. Its predictive power also diminishes for very large private companies (revenue beyond roughly ₹500 crore), where industry structure and capital complexity call for more granular analysis.

And it will never replace the interpretative half of this profession. Valuation is neither purely formula-driven nor purely intuitive — it must be both analytical and interpretative. GREV supplies the analytical anchor; the valuer supplies everything the data cannot see.

From numbers to confidence

The valuation of private companies is ultimately not about producing a number. It is about producing confidence in that number — for the board approving a transaction, the auditor reviewing a fair value, the regulator examining a filing, the investor wiring the money.

Indian valuation practice is institutionalising fast: IBBI registration, codified standards, rising judicial and regulatory scrutiny. The direction is clear — from judgment asserted to judgment evidenced. The GREV Model is my contribution to that shift: an India-specific, transaction-derived baseline that tells any valuer, in under a minute, whether their conclusion is having a conversation with the market or only with itself. Valuations are based on story and narratives, but that’s a high price to pay when billions are at stake. The evidence defends the price.

–

Dr. Vikash Goel, FCA, PhD (Valuation), CFA, MBA is the Managing Partner of Omnifin, a Registered Valuer Entity and valuation advisory firm. Omnifin advises on business valuation, IPO readiness, and cross-border transactions from offices in Kolkata, Mumbai, Ahmedabad, Gurgaon, and Bangalore. For valuation engagements, write to vg@omnifinsolutions.com.

The original doctoral thesis is available on Shodhganga at hdl.handle.net/10603/698267.

Another shorter version of this article can be found at LinkedIn Pulse