This NSE IPO valuation analysis is based on the DRHP filed with SEBI on 17 June 2026. Grey market pricing of ₹1,700–₹2,200 per share implies an equity value of roughly ₹4,95,000 crore at the midpoint — though our own NSE IPO valuation estimates, using both multiples and DCF methods, put fair value closer to ₹3,70,000–₹5,90,000 crore depending on methodology.

The National Stock Exchange (NSE) IPO has been a topic of conversation for a very long time now — discussed, debated, and delayed for nearly a decade since its earlier filing in 2016. There have been multiple transactions in the grey market already, and thousands of investors have picked up the stock from the private markets, eagerly waiting for the IPO to happen.

Now, with the DRHP formally filed with SEBI in June 2026, the conversation has moved from speculation to substance.

What is NSE’s expected IPO valuation?

Based on the DRHP filed with SEBI on 17 June 2026, grey market pricing of ₹1,700–₹2,200 per share implies an equity value of roughly ₹4,95,000 crore at the midpoint — though our own multiples and DCF-based estimates below put fair value closer to ₹3,70,000–₹5,90,000 crore depending on methodology.

IPO Structure

The IPO is entirely an Offer for Sale of up to 14.8 crore equity shares — approximately 6.02% of NSE’s paid-up capital of 247.5 Crore shares (face value INR 1, post 5:1 bonus). Not a single rupee goes to NSE itself. The selling shareholders include SBI, MS Strategic (Mauritius), Canada Pension Plan Investment Board, Aranda Investments (Temasek), Bank of Baroda, GIC Re, and others. Notably, LIC is not selling. The estimated OFS size of INR 25,000–30,000 crore would make this one of the largest public floats in Indian history.

The Value drivers

There is an obvious excitement for the IPO of NSE because of the nature of its business. Whether the markets go up or down, NSE is bound to make money. The fact that NSE has built an interesting infrastructure for the financial markets and operates with unique economics only adds to the excitement and sometimes the value of the stock. NSE is one of the most profitable exchange businesses in the world — a regulatory-moated, asset-light monopoly with 80%+ EBITDA margins.

- Network effects: The company benefits from powerful network effects. The more participants and exchange attract, the more valuable it becomes to every participant already on the platform. Liquidity attracts liquidity. NSE has already created a moat that is very difficult for any competitor to replicate in the medium to long run.

- Tech driven Operating Leverage: As an infrastructure business the company enjoys high operating leverage. NSE has invested significantly into world class technology, compliance, surveillance, cyber security, and risk management. Now that the infrastructure is established incremental transactions are processed at a very low additional cost. So, the company will continue to benefit from its already incurred cost and the margins are only expected to go up from here. As transaction volumes increase, profitability can expand disproportionately. The same benefits are enjoyed by companies like Amazon, Google, and Microsoft.

- India Capital Market story: India’s capital market have witnessed remarkable expansion over the last couple of decades. The rise and retail participation in the last decade, growth in mutual fund investments, increasing financial awareness, and digitization have collectively strengthened the foundations of the capital markets in India. We don’t see any possible decline in market participation in the coming years and the infrastructure providers such as NSE naturally stand to benefit from this trend.

- Professional Ops: People working closely with NSE will confirm that the company continues to operate in a fairly corporate and professional manner. While working with NSE staff during our IPO services with multiple companies, we have NSE providing impeccable customer service, market expansion and support that an infrastructure provider operating as a corporate entity should provide to its customers. This brings delight to IPO bound companies and adds value to NSE. Also, the company has been careful in managing its portfolio of different businesses.

- Global Financial Infra giant: ~51% of all equity derivatives contracts traded globally flow through NSE; 93% domestic cash market share (by total turnover); 7 consecutive years as the world’s largest derivatives exchange by contracts traded; 2,978 listed entities as at March 31, 2026

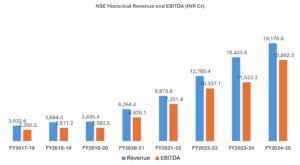

Numbers tell the story

- Revenue from Operations: INR 16,601 Cr (FY26), lower than FY25, due to SEBI-induced volume correction. general CAGR at ~15%

- EBITDA: The EBITDA Margins are at ~80% and is the highest amongst all global exchange groups.

- PAT: INR 10,302 Cr (FY26) vs INR 12,188 Cr (FY25). The 12.3% decline is almost entirely due to INR 1,432 Cr one-off SEBI settlement charge (co-location matter). Normalised PAT is INR 11,496 Cr.

- Dividends: The company paid INR 35 as Dividend per share including a special dividend.

NSE IPO Valuation: Multiples and DCF Analysis

The grey market price of NSE is already between INR 1700 and INR 2200. With 247.5 Crore shares, at an assumed price of INR 2000 per share, the Equity value translates to around INR 4,95,000 Crore. Let’s see if this price is justified.

But first, the disclaimers: This is an exercise for academic interest and is not a professional advise. Some of my family members or group entities may hold shares of NSE. The author or anyone from Omnifin is not responsible if you act /trade based on this article.

Multiples based valuation: Globally, the major indices such as CME group, LSE Group, SGX, Nasdaq etc. trade at a mean multiple of 22x EBITDA. BSE, on the other hand, trades at 48x EBITDA due to India growth story. The normalised FY26 EBITDA (after SEBI settlement costs) was ~INR 15,569 Crore. Assuming an FY27 EBITDA of ~INR 16,000 and a EBITDA Multiple of 22x translates into a Enterprise value (EV) of INR 352,000 Crore. However, if the multiple is closer to 35x (much lower than BSE’s 48x), the EV is INR 560,000 crore.

DCF Based Valuation.

Discount Rate: Our Discount rate is based on 7.24% Risk Free Rate (10 yr govt bond yield as on 31-Mar-26), Market Return of 11%, Beta of BSE at 0.80 and an additional risk premium of 1%. With Zero Debt, the Discount rate translates to 11.25%

Projections: Our projected cash flows are based on 15% growth in Revenues for 10 years with 81% EBIT Margins. The working Capital is negative, but we have assumed a 0.5% incremental Working Capital Investment ratio. The company operates with a lean model and Depreciation is expected to offset Capex. The tax rate is 25.17% and terminal growth rate is assumed at 5.5%, slightly higher than Omnifin’s standard private company terminal growth rate, given India’s high capital market growth potential.

Other Assets: NSE holds NSEIT, a Tech subsidiary, a stake in CAMS, NSE IFSC, among other portfolios. These are valued based on reported financials in DRHP.

| FY 26 Revenue (INR Cr) | 16,601.31 |

| Discount Rate (WACC) | 11.25% |

| 5-Year Growth Rate | 15.0% |

| Operating Expense as a % of Revenue | 19.0% |

| Perpetuity Growth Rate (After Year 5) | 5.5% |

| Tax Rate | 25.2% |

| WCIR | 0.5% |

| Projected D&A Per Year (INR Cr) | 500.0 |

| Capital Expenditures Per Year (INR Cr) | 500.0 |

The Valuation as per DCF translates into:

| Fiscal Year | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Terminal Value |

| Sales | 19,091.5 | 21,955.2 | 25,248.5 | 29,035.8 | 33,391.2 | 35,227.7 |

| % Growth | 15.0% | 15.0% | 15.0% | 15.0% | 15.0% | 5.5% |

| EBIT | 15,464.1 | 17,783.7 | 20,451.3 | 23,519.0 | 27,046.8 | 28,534.4 |

| % Margin | 81.0% | 81.0% | 81.0% | 81.0% | 81.0% | 81.0% |

| Taxes | (3,892.3) | (4,476.2) | (5,147.6) | (5,919.7) | (6,807.7) | (7,182.1) |

| NOPAT | 11,571.8 | 13,307.6 | 15,303.7 | 17,599.3 | 20,239.2 | 21,352.3 |

| Plus: D&A | 500.0 | 500.0 | 500.0 | 500.0 | 500.0 | 500.0 |

| Less: Change in WC | (12.5) | (14.3) | (16.5) | (18.9) | (21.8) | (9.2) |

| Less: CapEx | (500.0) | (500.0) | (500.0) | (500.0) | (500.0) | (500.0) |

| Free Cash Flow | 11,559.4 | 13,293.3 | 15,287.2 | 17,580.3 | 20,217.4 | 21,343.1 |

| Terminal Value | 3,71,184.8 | |||||

| PV of Cash Flows | 10,390.4 | 10,740.7 | 11,102.7 | 11,477.0 | 11,863.8 | 2,17,816.1 |

| Value of Operations (Enterprise Value) | 3,38,984.9 |

Here’s our summary of value

| EV/EBITDA | EV/EBITDA | DCF | |

| using 35x FY27 EBITDA of 16000 Cr; including India Premium | using 22x FY EBITDA of 16000 Cr; Industry mean multiple | WACC: 11.25%; Terminal Growth 5.5%; 15% Revenue Gr, 81% EBIT Margin | |

| Enterprise Value | 5,60,000.0 | 3,52,000.0 | 3,38,984.9 |

| Plus: Cash | 2,114.5 | 2,114.5 | 2,114.5 |

| Less: Debt | 0 | 0 | 0 |

| Plus: Other Assets | 28,814.5 | 28,814.5 | 28,814.5 |

| Equity Value (INR Cr) | 5,90,929.0 | 3,82,929.0 | 3,69,913.9 |

| No. of Shares (Cr) | 247.5 | 247.5 | 247.5 |

| Value per share (INR) | 2,388 | 1,547 | 1,495 |

The above are our base case assumptions in both scenarios. A more detailed estimate may result in significantly different values.

The NSE is one of the largest financial institutions in Indian history. The DRHP brings transparency to an institution that has operated as a quasi-public utility for over three decades, facilitated INR 20.33 lakh crore in fund mobilisation in FY2026 alone, and built a global franchise that few saw coming when trading went electronic in 1994.

Frequently Asked Questions

What is NSE’s expected IPO valuation?

Grey market pricing currently implies an equity value of around ₹4,95,000 crore at ₹2,000 per share. Our own analysis, using both EV/EBITDA multiples and a DCF model, estimates a range of roughly ₹3,70,000 crore to ₹5,90,000 crore depending on the methodology and multiple applied.

When will the NSE IPO list?

NSE filed its DRHP with SEBI on 17 June 2026. The price band, final issue size, and listing date will only be confirmed after SEBI’s observations and the subsequent RHP filing. NSE has targeted a listing before December 2026.

What is the NSE IPO price band?

Not yet announced. As the IPO is still at the DRHP stage, there’s no official price band — only grey market trading levels, currently around ₹1,700–₹2,200 per share.

Is the NSE IPO open for subscription now?

No. The IPO is in the DRHP review stage with SEBI. Subscription dates will be announced only after the RHP is filed and the price band is set.

Is the NSE IPO a fresh issue or an Offer for Sale?

Entirely an Offer for Sale (OFS) of up to 14.8 crore equity shares (~6% of paid-up capital). NSE itself receives no proceeds — all funds go to selling shareholders, including SBI, MS Strategic (Mauritius), CPPIB, and others.

Original Post: 18th June 2026 | Last Updated: 21 June 2026

Related Article:

Valuation of Razorpay , Valuation of SpaceX (LinkedIN)

About the author:

Dr Vikash Goel is the Founder and Managing Partner of Omnifin. He brings two decades of advisory experience to clients across India and North America. Prior to founding Omnifin, he spent a decade working with PwC and EY. He has authored multiple books on valuation and holds a Phd in Valuation. He is a CA, CFA, MS Finance, MBA, IIM Cal and a practicing IBBI Registered Valuer. He is also a SEBI Research Analyst. He can be reached at vg@omnifinsolutions.com

Connect with us for IPO Readiness or Valuation services

Disclaimer:

This article is for informational and educational purposes only. It does not constitute investment advice, a solicitation, or a recommendation to buy or sell any securities. The valuation analysis is based on publicly available DRHP data and Omnifin’s proprietary frameworks. Omnifin or author has not approved or endorsed this analysis. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult their financial advisors before making investment decisions